| |

Business opportunities for hardware in Industry 4.0

There is no denying the fact that smart manufacturing, which is best represented by the phenomenon of Industry 4.0, is changing the face of future manufacturing. Data is essential to this new manufacturing system. It is at the core. But this does not mean that hardware will be marginalized in Industry 4.0. After all, the value of data can only be presented in the physical world through hardware as a medium. Hence, the rise of “data” in smart manufacturing will bring precious business opportunities for hardware. Let us follow each step of the “data processes” in Industry 4.0 to observe the financial prospects of hardware at each phase.

Sensors

The word “robot” was not coined until the 20th century –

in a theatre play, “Rossum’s Universal Robots”, published

in 1920 by Czech author Karel Čapek. The drama is about

artificial humans – robots – who serve as cheap labour, devoid

of all rights, and ultimately rebel against their human

masters. It was not until the 1940s that the word “robot”

really became widespread, however, through the writings

of science-fiction author Isaac Asimov.

Initially used only to describe human-like machines, the

word “robot” today covers a wide range of different machinery.

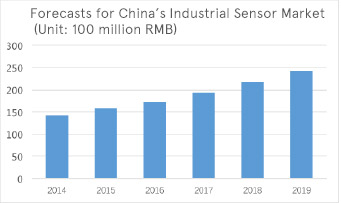

Figure 1: Forecasts for China’s Industrial Sensor Market

Growth of the CMOS image sensor market should also be noted since it is the core component of machine visuals. According to forecasts from IC Insights, the global industrial CMOS image sensor market will grow from USD396 million in 2015 to USD912 million in 2020. Even more image data can be collected through image sensors with the application of multi-view stereoscopic vision 3D technology, and more attention will be focused on the capabilities of image sensors, which has become a considerable slice of the pie in the industrial sensor market.

Networking

Data generated from smart manufacturing systems require a fast and reliable network for transmission and sharing. Germany’s Industry 4.0 white paper views wireless technology as an important part of research on network communication technology in Industry 4.0. Wireless communication technology has clear advantages over traditional wired communication technology: 1. Low cost of network construction and maintenance; calculations show that control systems that use wireless technology can reduce installation and maintenance costs by 90%. 2. More flexible layout of equipment in the production line, in order to better meet the flexibility requirements under the vision of mass customization under smart manufacturing. 3. Adaptable to diverse network application scenarios, as well as deployment of mesh, star and other types of networks.

Hence, whether it may be pre-existing wireless protocols in the industry, e.g. WIA-PA, Wireless HART, and ISA, or general wireless protocols, e.g. WiFi, Zigbee, NFC, Bluetooth, and 2G/3G/4G mobile communications,

wireless technology is making inroads in the industrial sector. A number of companies are currently considering how to incorporate emerging LPWAN wireless communication technologies, such as NB-IoT, into industrial applications. The development of 5G is also within the scope of Industry 4.0, and the design and standards for public 5G network infrastructure will be realized in 2018 as planned, providing WAN service for the industrial sector.

Industrial applications, however, have special requirements regarding wireless communications, especially when it comes to reliability and low latency. Hence, general wireless technologies will still be mainly used in situations not requiring real-time control, such as equipment and product information gathering or internal information exchange, and will form compound communications systems with the real-time industrial control network, establishing a high performance, reliable data channel.

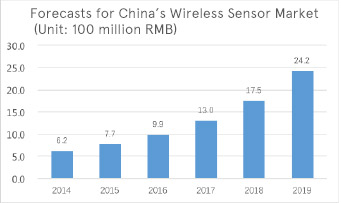

At present, wireless connection and sensor technologies are also being integrated, and wireless sensors with the ability to transmit data wirelessly will become a new source of market growth. A wireless sensor network established on this basis will be free from the restraints of bus bars for traditional sensors, and make data collection more flexible and cheaper. In the case of China’s market, the market scale of industrial wireless sensors was RMB620 million in 2014, accounting for roughly 4.3% of the overall industrial sensor market in China; the market scale of industrial wireless sensors will reach RMB2.42 billion in 2019 and account for 10% of the overall industrial sensor market, reaching a compound annual growth rate of 27.1%. Sensor products can even be combined with other technologies, such as energy harvesting, to create even more diverse products and expand their applications.

Figure 2: Forecasts for China’s Wireless Sensor Market

Even though the blueprint for wireless communications can be very exciting, wired communications remains indispensable in the industrial sector, especially for industrial data transmission applications that require wide bandwidth, high reliability, and rapid response. This has created demand for high performance, highly reliable industrial connectors. Connector manufacturers have spared no effort in a market with such high added value. For example, a M8/M12 connector can now support data rates of up to 1Gbps.

Unlike consumer markets, industrial markets can usually provide hardware manufacturers with stable and high profit margins. To learn exactly what kind of surprises will be brought by the trend of smart manufacturing.

In the complete closed-loop processes typical of smart manufacturing, the three key links that need to be completed in the data-driven process are sensing, decision making, and execution. A high-performance, reliable network must also be in place for data communication and exchange. Next we are going to focus on the surprises that hardware will have in the decision-making and execution process.

Data-driven decision-making

Collecting data into the cloud for analysis and processing, as well as exchange with existing knowledge bases for decision-making is the core process of Industry 4.0. This will naturally drive increasing demand for data centers among industrial applications, whether it uses the public cloud or building a private cloud, the total number of data centers will inevitably increase. The scale of the global data center infrastructure market is expected to reach USD44 billion in 2019.

In response to the growingly heavy burden of big data processing tasks, even more powerful processors will be needed in the future. A new type of heterogeneous processor architecture is currently making its way into the spotlight to resolve the processing bottleneck encountered by generic multi-core processors. Developers are considering a CPU+GPU model to maximize the floating-point processing capabilities of a GPU. Field programmable gate arrays (FPGA) are also attracting attention, and they have the potential to become the mainstream processing architecture for data center servers of the future after integration with generic processors. Intel, the leader of the server processor market, acquiring Altera, the second largest FPGA manufacturer in the world, proves this trend. Qualcomm announced that it formed an alliance with Xilinx, the largest FPGA manufacturer in the world, and Mellanox shortly after, so as to compete with Intel. Hence, we can look forward to future developments of the data center core processor market.

It should be noted that the power consumption of data center will continue to reach new heights as processing ability continues its rapid rise. According to data from 2015, there were over 3 million data centers around the world, and their power consumption had already reached 1.1%-1.5% of global power consumption. If we look into the operating costs of a single data center, the electricity bill accounts for 70% of expenses, far exceeding the cost of infrastructure, so there is a great demand for reducing power consumption in data centers. This is why the power structure of data centers is currently being reformed, such as using a central transformer to transform AC into 380V DC, which is then distributed to power consuming units through a high voltage DC bus bar, simplifying the structure and improving its efficiency. A similar reform created market opportunities for data center related power managers. According to reports, the market scale of data center reform was roughly RMB3 billion in 2015, and is expected to continue growing in the next 5 years.

Execution

After data is analyzed and processed in the cloud, the decision command will be returned to the executing device and become a mechanical action, forming a complete closed-loop process of control “from device to cloud, and from cloud to device.” All mechanical operations in the manufacturing industry are electric machine driven, so precision electric machine control will become a new source of market growth induced by Industry 4.0. From a hardware perspective, this will provide opportunities for core digital control chips, such as MCU, DSP, and FPGA.

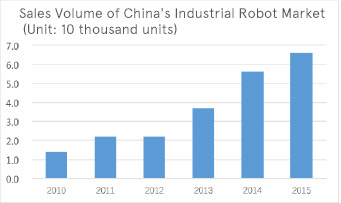

Figure 3: Rapid Growth of China’s Industrial Robot Market After 2010

Industrial robots must be mentioned when it comes to Industry 4.0 as they are a smarter, universal execution device. A total of 240 thousand industrial robots were sold around the world in 2015 with an annual growth rate of 15% over the last five years. The industrial robot market in China grew by a stunning 35% each year from 2010 to 2015 to a total of 66 thousand industrial robots. At this rate, China will account for 40% of the global industrial robot market by 2020. The markets for the core components of industrial robots—server systems, reducers, and controllers—all grew along with the industrial robot market. In the industrial robot controller market, particularly, the industry realized that the closed systems designed and developed by robot manufacturers were no longer able to meet the demand of a rapidly development market, and standardization and openness are now becoming trends. A few independent manufacturers of robot controllers are becoming more active in the market, and we shall wait and see if they can use the market’s power to change the ecology of the industrial robot industry.

In summary, the data-driven reform of Industry 4.0 does not simply bring linear product changes in the manufacturing industry, but rather creates new structures, new product categories, and new models. What we see today is merely one facet, and the whole picture of business opportunities for hardware will only be revealed if we dig deeper into future market developments.

▲TOP

|

|

|